Closely following market sentiment, especially negative market views – falling share prices, widening CDS spreads etc – can be very helpful in bringing latent issues about a company to our attention. However, as the Wall Street Journal highlighted recently: “There is no substitute for fundamental research.”

This was the opening sentence in the Journal’s coverage of Melinta Therapeutics, the New Jersey biopharmaceutical firm, whose shares lost two thirds of their market value the day after the company announced it was filing for bankruptcy on 2 January 2020. The journalist pointed out that management had given investors warning in Melinta’s 10Q SEC filing on 12 November 2019 that explicitly stated:

“….. while we continue to evaluate alternatives to address our liabilities outside of a bankruptcy process, it likely will be necessary for us to commence proceedings under Chapter 11 of the U.S. Bankruptcy Code, and we anticipate that, in any such Chapter 11 proceedings, holders of our equity securities (or claims and interests with respect to, or rights to acquire, our equity securities) would be entitled to little or no recovery, and those claims and interests may be cancelled for little or no consideration. If that were to occur, we anticipate that all or substantially all of the value of all investments in our equity securities would be lost and that our equity holders would lose all or substantially all of their investment.”

Perpetually in search of early warning indicators of pending distress, we do well tracking prices and spreads to get a sense of market sentiment. So when events like this occur we ask ourselves: Markets are supposed to be efficient; how could this happen? How could so many have missed this clearly sign-posted warning?

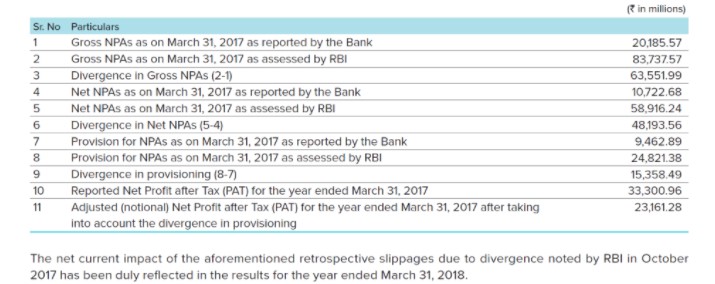

For those of us who cover banks, there is an analogy to this story. When Yes Bank, published its 31-3-2018 year end accounts it would appear that few investors took note of the disclosure in the notes to the accounts which showed that the bank had substantially under reported Non-Performing Assets (NPAs). The additional net NPA’s – as assessed by the Reserve Bank of India (RBI) – amounted to ~18% of book capital. (Balance sheet equity was Rs 257,525 million at year end.) See extract below.

Despite being fined and publicly criticized for under reporting NPAs in 2016 and 2017, Yes Bank’s share price in mid-August 2018 reached an all-time high of Rs 393. The share price began its precipitous fall the day after the bank’s 20 September 2018 Stock Exchange announcement that Reserve Bank of India (RBI) had refused Yes Bank’s board’s request to extend Rana Kapoor’s term as chief executive until 2021 but insisted that it end January 2019. (Mr Kapoor was co-founder as well as CEO of Yes Bank) The shares fell to Rs226 on 21 September 2018. The challenges for the bank sadly continued, the bank was unable to raise new capital, as its share price collapsed.

Yes Bank Share Price Graph

Source: BSE https://economictimes.indiatimes.com/yes-bank-ltd/prices/companyid-16552.cms

Alas, the story has now come to an end, on 6 March 2020 RBI announced that a rescue has been arranged: State Bank of India would inject Rs 75.2 billion ($975 million) for a 49% stake in Yes Bank, as part of the central bank’s resolution plan. The plan includes the cancellation of Rs 108 billion ($1.5billion) AT1 bonds. While the solution was being hammered out, deposit withdrawals were limited to Rs 50K ($670) per person. A sad ending for a bank that was valued at $13.4 billion at its peak in 2017.

The lesson learned? To do our jobs well, we need to both closely track market trends and be timely in our review of the quarterly, as well as year–end results of the firms we follow.

Source: FT 14 March 2020